Clarksons looks at car carrier trade trends

Written by Nick Blenkey

Last week brought a slew of reports about ever larger car carriers being ordered and designed.

What’s all the buzz about? Despite electric vehicle sales disappointing automakers this year, a surge in global demand is still being forecast — and, with it, a surge in demand for car carrier capacity. Forbes has some interesting analysis on what this means for the auto industry. Meantime, for the marine industry, recent car carrier trade trends provide some insights and Clarksons Research’s David Whittaker has released some highlights from Clarkson’s Car Carrier Trade & Transport 2023 report.

Whittaker says that the driving force behind the car carrier sector this year has been exceptional trade growth and the shipping demand this has created.

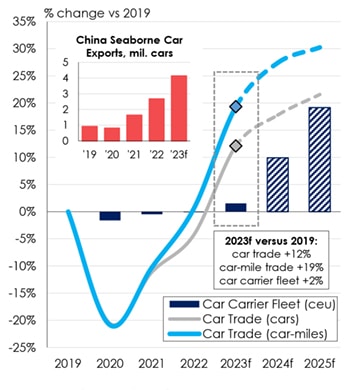

“We project global ‘deep sea’ seaborne car trade will grow by 17% to 23.7 million cars, smashing past the ‘pre-Covid’ record of 21.5 million cars set in 2018 as Chinese exports continue to surge (>4 million cars this year) and production in other key regions recovers from component shortages which held back volumes in 2021-22,” says Whittaker. “Surging China- Europe volumes also mean that ‘car- mile’ trade is set to grow by an even firmer 19% this year. Overall, car trade volumes are on track to stand 12% above pre-Covid levels this year, and 19% above in car-miles (see graph). Other factors including strong ‘high and heavy’ volumes and the growing share of trade accounted for by generally larger and heavier EVs and hybrids (29% this year, up from 9% in 2019) have further ‘turbocharged’ vessel demand. These trade trends ‘dwarf’ modest fleet expansion of just ~2% since 2019.”

Whittaker says that operators have generally reported strong (and in some cases, record) financial results this year, while charter rates are at record levels.

“Our guideline one year time charter rate for a ~6,500 CEU PCTC stood at $115,000/day by November, up a further 10% from already record year-ago levels,” says Whittaker.

Whittaker notes that newbuild ordering in the sector has continued apace in 2023. Latest data shows that 80 vessels of 677,000 CEU have now been confirmed ordered in 2023, he says, a new annual record, that takes the orderbook to ~37% of fleet capacity. Around 85% of capacity on order is set to be alternative fuel capable (mostly LNG, some methanol), while 28% of ca- pacity is ammonia or methanol “ready.”

Operators have led newbuild ordering activity this year, while Chinese yards are set to build the vast majority (~85%) of capacity now on order.