Rate of newbuild ordering slows in second quarter

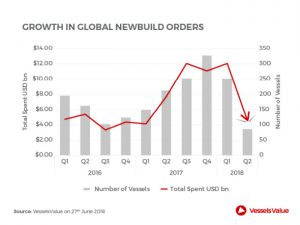

JULY 10, 2018 —Newbuilding orders slowed across all major ship types in the second quarter of this year, after over $10 billion was committed in the first quarter, according to VesselsValue’s analyst

JULY 10, 2018 —Newbuilding orders slowed across all major ship types in the second quarter of this year, after over $10 billion was committed in the first quarter, according to VesselsValue’s analyst

MAY 1, 2018 — VesselsValue (VV), the world’s leading online valuation provider, is launching daily valuations for Offshore Construction Vessels (OCVs). This completes VV’s expansion into Offshore Valuation, which already includes all

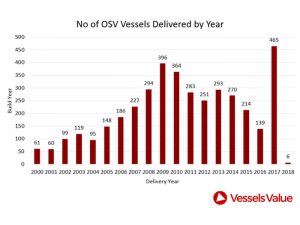

MARCH 27, 2018 — VesselsValue reports that operators of offshore service vessels are beginning to scrap an increasing number of older vessels, with year-to-date scrapping rates increasing by 153 percent on the

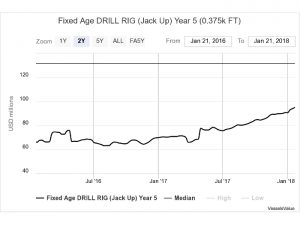

JANUARY 26, 2018 —Rising oil prices have increased interest in secondhand for jack-up rigs, pushing asset values up 36 percent from a year ago, according to data compiled by VesselsValue. VV’s Fixed

JULY 25, 2017—While the number of orders for new vessels declined in the first half of 2017 as compared with 2016, the number of bulkers and tankers order rose, according to data

MAY 8, 2017 — The global OSV fleet’s Discounted Cash Flow (DCF) value is currently $79.9 billion, or 2.5 times higher than its current market value of $30.9 billion, according to VesselsValue

MARCH 8, 2017 — Figures from VesselsValue indicate that the oversupply of vessels in the offshore services industry is set to get a lot worse. VesselsValue says that 2017 will be a

As we pointed out in our Annual Yearbook & Maritime Review back in June, shipyards are struggling amid the downturn in the market, with newbuilding orders at their lowest levels since the 1980s. As further evidence, during the first half of 2016, orders for new ships worldwide dropped 65 percent as compared with the first half of last year, according to VesselsValue.

The leading ship valuation provider says that 689 newbuilds were ordered in the first half of 2015 as compared with a mere 239 this year.

As we mark the midway part of this year, VesselsValue also points out that $28.4 billion worth of vessels have been delivered this year, with another $43.8 billion worth still on the orderbooks and due for delivery in 2016. VesselsValue says that there a total of 2,518 vessels to be built in 2016, with 1,613 as yet undelivered by mid-year. Almost a third of the undelivered vessels are bulkers.

LPG tanker deliveries are on track for the year, with 50% of the 2016 orderbook having been delivered (worth $3.0 billion). However there is still 80% of the Offshore Support Vessel (OSV) orderbook still undelivered, valued at $5.5 billion. Overall, only 93 of the 500 OSVs on order were delivered to the fleet this year. VesselsValue Valuation Analysts say many of the undelivered vessels in underperforming markets are candidates for slippage: the vessel’s delivery date may be pushed back into the next few years.

The tanker outlook

Updating its Mid-Year Tanker Market Outlook, McQuilling Services says that 49 uncoated tankers were delivered at the end of July, representing “36% of our full-year expectations and supporting our original thoughts of a second half skew of tanker deliveries.” McQuilling Services sees the supply outlook over the next five years as a “tale of two halves.” It says the present year along with 2017 are projected to increase the DPP fleet as a whole by 3.6% and 5.7% on an average inventory basis. In total, we project 62 coated Aframaxes (LR2) and 46 coated Panamaxes (LR1) to join the fleet over 2016 and 2017, of which 27 have delivered as of August.

McQuilling Services says, “We anticipate that LR2 inventory will expand 10.7% and 9.9% in 2016 and 2017, respectively amid high deliveries and minimal deletions, while the MR product segment is to average only 1.0% growth through 2020. Overall, Clean Petroleum Products (CPP) growth will average 3.5% in 2016 before trending lower over the forecast period. The net fleet growth of the chemical fleet (IMO 2) is projected to expand by 13.5% in 2016, reducing to 3.4% in 2018 and below 2.0% in 2019 and 2020.

“We project spot rates for Dirty Petroleum Products (DPP) voyages to exhibit weakness in 2017 amid accelerating supply growth. TD3 freight rates will average WS 57 in 2017 before increasing to WS 71 by 2020. Floating storage economics may help stabilize the recent downturn in the market. Correspondingly, we anticipate VLCC TCE levels to average $33,800/day in 2017. Suezmax rates on TD20 are projected to average WS 66 in 2017, returning owners $15,300/day during the year. Aframax rates are likely to be elevated in the East with TD8 returning owners $19,600/day in 2017, following $22,300/day in 2016.”

According to McQuilling, CPP rates are likely to remain stable in 2017 due to increasing demand and decelerating supply. TC1 rates will average WS 108 in 2017, returning owners $19,200/day, while the LR1 trading the same voyage will generate earnings of $13,800/day. Gradually increasing freight rates through 2020 are projected. For MR owners, it is projected that vessels positioned in Asia will earn more than those in the West amid expanding refinery capacity in the East and slowing demand in the West. The TC2/TC14 triangulation will return owners $11,806/day in 2017.

Asset prices for secondhand DPP tankers will see losses continue into 2017 amid a weakening rate environment, while CPP values may see a slight uptick amid a more stable earnings outlook. Declining shipyard capacity and higher commodity prices may lead to a slight increase in newbuilding values next year.

Cruise market booming

The cruise ship market is booming, with orders for more than 60 cruise vessels valued at over $44 billion, including two 100-passenger coastal cruise ships being built at Nichols Brothers Boat Builders, Whidbey Island, WA, and two overnight cruise ships at Chesapeake Shipbuilding in Salisbury, MD. Chesapeake delivered the 185-passenger America to its sister company American Cruise Line in the first quarter of this year.

Matson orders two CONROs

In the U.S., orders for the first half of 2016 for new oceangoing ships for Jones Act trade have slowed, with shipyards working off their existing backlogs. The second half of the year started off with a bang as Matson Navigation awarded a $511 million contract to General Dynamics NASSCO, San Diego, CA, last month for two new LNG-Ready Container Roll-on/Roll-Off (CONRO) vessels that will have a capacity of 3,500 TEU. The two CONROs would be the 30th and 31st LNG-powered or LNG-Ready ships built, in operation, under construction or conversion for Jones Act service.

The birth of VesselsValue was driven by timing and need. In 2008, the crisis in the financial market extended into shipping. The dry bulk sector and the containership sector were hit the hardest, and while tankers remained relatively buoyant, banks needed to assess their capital commitments against the value of the assets being financed and being used as collateral. However, in the depth of the crisis (2010 / 2011), ship brokers were telling clients they could not value the ships as there had been no recent sale or “last done” in ship broker speak. Richard Rivlin, a sale and purchase broker with 30 years’ experience, had long felt that an automatic valuation system could be built, which would produce valuations in any market, at any time. Luckily, his brother is a Professor of Mathematics, and together they designed and built such a system. It quickly became apparent that the highly detailed multi-level regression model was far too complex for normal spreadsheets, and a specialist modelling company was employed to develop the model.

The model is fed by two databases. One contains the features and specification of the ships arranged in a unique structure that allows the computational model high speed access. This database is researched and compiled by VesselsValue own team of 30 researchers and analysts on the Isle of Wight in the UK. The second database consists of sale and purchase transactions and charters. Both feed the mathematic model which is operated by a team of quantitative analysts. The aim was to produce an instant, accurate and always available online ship valuations for the banks and finance houses, that form the main customers of VesselsValue.

Tankers Valuation

According to VesselsValue, five factors make up a valuation:

Each factor is broken down into further elements that are scored. As an asset, tankers are relatively straightforward, being highly commoditized, and standardized in terms of size ranges and specification. In part this is due to the international safety and pollution control legislation that has been forced on the tanker sector. This level of standardization makes VesselsValue task somewhat easier when it comes to scoring the factors, than offshore vessels, which have just been added to the system. In the case of tankers, there are around 140 scores. One of the most important scores is the shipyard. A vessel built in China is less desirable than one built in Japan. A well-published example is the one shown above. In November 2014, the New Century-built Supramax bulker ACS Diamond was sold for $10 million. The previous week, the slightly older Japanese-built pair of Supramaxes were sold for $15.5 million each. This was an implied discount of around 40% between Japan and China. However, the shipyard scoring goes into several levels of sophistication, including many ships the shipyard has built and when the last vessel was constructed.

This model is continually updated and recalibrated overnight to give the closest possible fit to the reported sales prices. It is the analysis of the sales that can produce the weightings required for different shipyards. These are applied to all shipyards, not just Chinese shipyards.

So far VesselsValue have performed over 1,000,000 valuations to date, about 400,000 a year and the number is increasing.

How Accurate is VesselsValue?

The split of VV customers are banks and finance houses, owners and other maritime industries such as lawyers, insurers and charterers – sophisticated market participants who insist on knowing the methodology behind our valuations. But ultimately they want to know how accurate are our valuations because this will affect their bottom line. Valuation accuracy is assessed as the difference between the price a vessel is sold at, and VV valuation on the day before the actual sales date. This is expressed as a % of valuations within a certain band of accuracy and shown in a chart form. The accuracy report is available on the website.

Tanker Valuations Development

According to the VesselsValue transactions database, between the start of 2012 and May 2016, a total value of $143 billion of tankers have been traded on the sale and purchase market. During that period the value of second-hand tankers has steadily increased, as can be seen from figure 1 (“VV Tanker Matrix”) below of the VV Tanker Matrix, expressed as USD / DWT.

During that period, the MR tanker has been the most frequently traded tanker type, both in terms of number of sales, and value (see figure 2 “Total Value by Type of Tankers Sold 2012 to Date”).

So far in 2016 (to 15 May 2016) 83 tankers with a total value of $1.4 billion, have been traded on the second-hand market, and again the MR tanker is the most popular (see figure 3 “Value of Tankers Sales Jan 2016 to YTD).

Interestingly, the average age of MR2 (Chemical / Product) tankers sold in the first five and half months of 2016 is only three years-old. Altogether 17 of these vessels were sold in this period, with eight tankers being sold by owners in the USA (these were not Jones Act vessels).

The majority of tankers and the largest value of tankers sold so far this year (2016) were constructed in South Korea, followed by Japan and China. As far as owners are concerned, the lead seller across all types of tankers was Chembulk Tankers, Scorpio Tankers and companies associated with the Navig8 group (see figure 4 “Top Ten Sellers of Tankers Ranked by Number of Vessels Sold”).

Recent Sales of Interest

The top three sellers have sold tankers for completely different reasons and strategy. In January 2016, Chembulk Tankers was sold by parent company Berlian Laju Tanker (BLT) to private equity investor Kohlberg Kravis Roberts (KKR). Chembulk Tankers is said to have a number of Contracts of Affreightments (CoAs) and the older tankers were surplus to requirement. This is part of the KKR growth strategy to rebuild the Chembulk Tankers fleet. KKR has also invested in a fund to invest in two Greek bank shipping portfolios.

The number two top seller, Scorpio Tankers, was a tactical, opportunistic sale. The purchaser, Bahri (formerly known as National Chemical Carriers of Saudi Arabia) is on something of a buying spree. Bahri has recently purchased two VLCCs from Tanker Investments in December 2015, for a reported $77.5 million. The five 2014-built MR2 tankers were sold en bloc for $167 million are trading in the UAE under Bahri CoAs.

The third most active seller, Navig8 Chemical Tankers, Inc., sold the four resales (the MR2 tankers are due for delivery in 2017) under a ten-year bareboat charter (with purchase option) for a reported $35 million each. This was an internal sale within the group, and part of a longer term strategy.

JUNE 15, 2016—Billionaire Greek shipping magnate John Angelicoussis was the biggest spender at the recently concluded Posidonia 2016 Exhibition in Athens. Angelicoussis, owner of Angelicoussis Shipping Group, which includes Anagel Maritime Services,